(ii) A proposal which will increase the after tax proceeds from the sale of the Snapper plc loan stock and a

reasoned recommendation of a more appropriate form. of external finance. (3 marks)

第1题:

(c) (i) State the date by which Thai Curry Ltd’s self-assessment corporation tax return for the year ended

30 September 2005 should be submitted, and advise the company of the penalties that will be due if

the return is not submitted until 31 May 2007. (3 marks)

(ii) State the date by which Thai Curry Ltd’s corporation tax liability for the year ended 30 September 2005

should be paid, and advise the company of the interest that will be due if the liability is not paid until

31 May 2007. (3 marks)

(c) Self-assessment tax return

(1) Thai Curry Ltd’s self-assessment corporation tax return for the year ended 30 September 2005 must be submitted by

30 September 2006.

(2) If the company does not submit its self-assessment tax return until 31 May 2007, then there will be an automatic fixed

penalty of £200 since the return is more than three months late.

(3) There will also be an additional corporation tax related penalty of £4,415 (44,150 × 10%) being 10% of the tax unpaid,

since the self-assessment tax return is more than six months late.

Corporation tax liability

(1) Thai Curry Ltd’s corporation tax liability for the year ended 30 September 2005 must be paid by 1 July 2006.

(2) If the company does not pay its corporation tax until 31 May 2007, then interest of £3,035 (44,150 at 7·5% = 3,311

× 11/12) will be charged by HM Revenue & Customs for the period 1 July 2006 to 31 May 2007.

第2题:

(c) Assuming that Stuart:

(i) purchased 201,000 shares in Omega plc on 3 December 2005; and

(ii) dies on 20 December 2007,

calculate the potential inheritance tax (IHT) liability which would arise if Rebecca were to die on 1 March

2008, and no further tax planning measures were taken.

Assume that all asset values remain unchanged and that the current rates of inheritance tax continue to

apply. (6 marks)

第3题:

(ii) the recent financial performance of Merton plc from a shareholder perspective. Clearly identify any

issues that you consider should be brought to the attention of the ordinary shareholders. (15 marks)

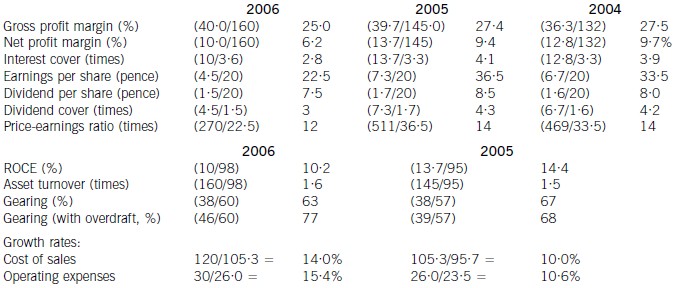

(ii) Discussion of financial performance

It is clear that 2006 has been a difficult year for Merton plc. There are very few areas of interest to shareholders where

anything positive can be found to say.

Profitability

Return on capital employed has declined from 14·4% in 2005, which compared favourably with the sector average of

12%, to 10·2% in 2006. Since asset turnover has improved from 1·5 to 1·6 in the same period, the cause of the decline

is falling profitability. Gross profit margin has fallen each year from 27·5% in 2004 to 25% in 2006, equal to the sector

average, despite an overall increase in turnover during the period of 10% per year. Merton plc has been unable to keep

cost of sales increases (14% in 2006 and 10% in 2005) below the increases in turnover. Net profit margin has declined

over the same period from 9·7% to 6·2%, compared to the sector average of 8%, because of substantial increases in

operating expenses (15·4% in 2006 and 10·6% in 2005). There is a pressing need here for Merton plc to bring cost

of sales and operating costs under control in order to improve profitability.

Gearing and financial risk

Gearing as measured by debt/equity has fallen from 67% (2005) to 63% (2006) because of an increase in

shareholders’ funds through retained profits. Over the same period the overdraft has increased from £1m to £8m and

cash balances have fallen from £16m to £1m. This is a net movement of £22m. If the overdraft is included, gearing

has increased to 77% rather than falling to 63%.

None of these gearing levels compare favourably with the average gearing for the sector of 50%. If we consider the large

increase in the overdraft, financial risk has clearly increased during the period. This is also evidenced by the decline in

interest cover from 4·1 (2005) to 2·8 (2006) as operating profit has fallen and interest paid has increased. In each year

interest cover has been below the sector average of eight and the current level of 2·8 is dangerously low.

Share price

As the return required by equity investors increases with increasing financial risk, continued increases in the overdraft

will exert downward pressure on the company’s share price and further reductions may be expected.

Investor ratios

Earnings per share, dividend per share and dividend cover have all declined from 2005 to 2006. The cut in the dividend

per share from 8·5 pence per share to 7·5 pence per share is especially worrying. Although in its announcement the

company claimed that dividend growth and share price growth was expected, it could have chosen to maintain the

dividend, if it felt that the current poor performance was only temporary. By cutting the dividend it could be signalling

that it expects the poor performance to continue. Shareholders have no guarantee as to the level of future dividends.

This view could be shared by the market, which might explain why the price-earnings ratio has fallen from 14 times to

12 times.

Financing strategy

Merton plc has experienced an increase in fixed assets over the last period of £10m and an increase in stocks and

debtors of £21m. These increases have been financed by a decline in cash (£15m), an increase in the overdraft (£7m)

and an increase in trade credit (£6m). The company is following an aggressive strategy of financing long-term

investment from short-term sources. This is very risky, since if the overdraft needed to be repaid, the company would

have great difficulty in raising the funds required.

A further financing issue relates to redemption of the existing debentures. The 10% debentures are due to be redeemed

in two years’ time and Merton plc will need to find £13m in order to do this. It does not appear that this sum can be

raised internally. While it is possible that refinancing with debt paying a lower rate of interest may be possible, the low

level of interest cover may cause concern to potential providers of debt finance, resulting in a higher rate of interest. The

Finance Director of Merton plc needs to consider the redemption problem now, as thought is currently being given to

raising a substantial amount of new equity finance. This financing choice may not be available again in the near future,

forcing the company to look to debt finance as a way of effecting redemption.

Overtrading

The evidence produced by the financial analysis above is that Merton plc is showing some symptoms of overtrading

(undercapitalisation). The board are suggesting a rights issue as a way of financing an expansion of business, but it is

possible that a rights issue will be needed to deal with the overtrading problem. This is a further financing issue requiring

consideration in addition to the redemption of debentures mentioned earlier.

Conclusion

Ordinary shareholders need to be aware of the following issues.

1. Profitability has fallen over the last year due to poor cost control

2. A substantial increase in the overdraft over the last year has caused gearing to increase

3. It is possible that the share price will continue to fall

4. The dividend cut may warn of continuing poor performance in the future

5. A total of £13m of debentures need redeeming in two year’s time

6. A large amount of new finance is needed for working capital and debenture redemption

Appendix: Analysis of key ratios and financial information

第4题:

(ii) Advise Benny of the amount of tax he could save by delaying the sale of the shares by 30 days. For the

purposes of this part, you may assume that the benefit in respect of the furnished flat is £11,800 per

year. (3 marks)

第5题:

(ii) Explain the income tax (IT), national insurance (NIC) and capital gains tax (CGT) implications arising on

the grant to and exercise by an employee of an option to buy shares in an unapproved share option

scheme and on the subsequent sale of these shares. State clearly how these would apply in Henry’s

case. (8 marks)

第6题:

(c) the deferred tax implications (with suitable calculations) for the company which arise from the recognition

of a remuneration expense for the directors’ share options. (7 marks)

第7题:

(ii) Illustrate the benefit of revising the corporate structure by calculating the corporation tax (CT) payable

for the year ended 31 March 2006, on the assumptions that:

(1) no action is taken; and

(2) an amended structure as recommended in (i) above is implemented from 1 June 2005. (3 marks)

第8题:

(b) Explain the meaning of the term ‘Efficient Market Hypothesis’ and discuss the implications for a company if

the stock market on which it is listed has been found to be semi-strong form. efficient. (9 marks)

第9题:

(c) Without changing the advice you have given in (b), or varying the terms of Luke’s will, explain how Mabel

could further reduce her eventual inheritance tax liability and quantify the tax saving that could be made.

(3 marks)

The increase in the retail prices index from April 1984 to April 1998 is 84%.

You should assume that the rates and allowances for the tax year 2005/06 will continue to apply for the

foreseeable future.

第10题:

(ii) Compute the annual income tax saving from your recommendation in (i) above as compared with the

situation where Cindy retains both the property and the shares. Identify any other tax implications

arising from your recommendation. Your answer should consider all relevant taxes. (3 marks)