A financial customer has three data centers that are four kilometers apart. Their SAP application data needs to be kept synchronized within 10 milliseconds. Which solution satisfies the customer’s recovery time objective()

第1题:

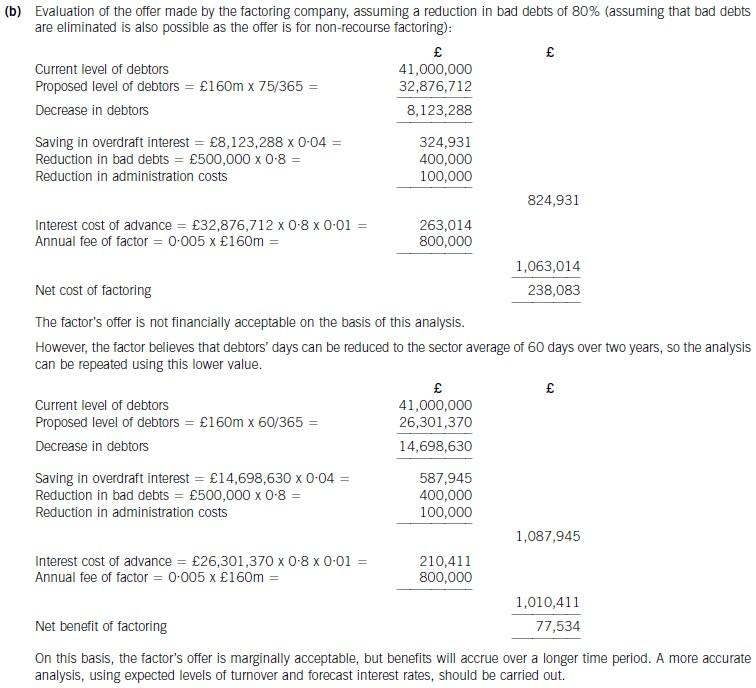

(b) Determine whether the factoring company’s offer can be recommended on financial grounds. Assume a

working year of 365 days and base your analysis on financial information for 2006. (8 marks)

第2题:

(b) Prepare a consolidated statement of financial position of the Ribby Group at 31 May 2008 in accordance

with International Financial Reporting Standards. (35 marks)

第3题:

In the opinion of most parents, .

A. economics should be the focus of school teaching

B. more students should be admitted to universities

C. the teaching of financial matters should be strengthened.

D. children should solve financial problems themselves

第4题:

It can be inferred from the last paragraph that

A.financial risks tend to outweigh political risks.

B.the middle class may face greater political challenges.

C.financial problems may bring about political problems.

D.financial responsibility is an indicator of political status.

第5题:

(b) Discuss the relative costs to the preparer and benefits to the users of financial statements of increased

disclosure of information in financial statements. (14 marks)

Quality of discussion and reasoning. (2 marks)

第6题:

(b) Describe with suitable calculations how the goodwill arising on the acquisition of Briars will be dealt with in

the group financial statements and how the loan to Briars should be treated in the financial statements of

Briars for the year ended 31 May 2006. (9 marks)

(b) IAS21 ‘The Effects of Changes in Foreign Exchange Rates’ requires goodwill arising on the acquisition of a foreign operation

and fair value adjustments to acquired assets and liabilities to be treated as belonging to the foreign operation. They should

be expressed in the functional currency of the foreign operation and translated at the closing rate at each balance sheet date.

Effectively goodwill is treated as a foreign currency asset which is retranslated at the closing rate. In this case the goodwillarising on the acquisition of Briars would be treated as follows:

At 31 May 2006, the goodwill will be retranslated at 2·5 euros to the dollar to give a figure of $4·4 million. Therefore this

will be the figure for goodwill in the balance sheet and an exchange loss of $1·4 million recorded in equity (translation

reserve). The impairment of goodwill will be expensed in profit or loss to the value of $1·2 million. (The closing rate has been

used to translate the impairment; however, there may be an argument for using the average rate.)

The loan to Briars will effectively be classed as a financial liability measured at amortised cost. It is the default category for

financial liabilities that do not meet the definition of financial liabilities at fair value through profit or loss. For most entities,

most financial liabilities will fall into this category. When a financial liability is recognised initially in the balance sheet, the

liability is measured at fair value. Fair value is the amount for which a liability can be settled, between knowledgeable, willing

parties in an arm’s length transaction. In other words, fair value is an actual or estimated transaction price on the reporting

date for a transaction taking place between unrelated parties that have adequate information about the asset or liability being

measured.

Since fair value is a market transaction price, on initial recognition fair value generally is assumed to equal the amount of

consideration paid or received for the financial asset or financial liability. Accordingly, IAS39 specifies that the best evidence

of the fair value of a financial instrument at initial recognition generally is the transaction price. However for longer-term

receivables or payables that do not pay interest or pay a below-market interest, IAS39 does require measurement initially at

the present value of the cash flows to be received or paid.

Thus in Briars financial statements the following entries will be made:

第7题:

(b) Discuss how management’s judgement and the financial reporting infrastructure of a country can have a

significant impact on financial statements prepared under IFRS. (6 marks)

Appropriateness and quality of discussion. (2 marks)

第8题:

It can be inferred from the last paragraph that

[A] financial risks tend to outweigh political risks.

[B] the middle class may face greater political challenges.

[C] financial problems may bring about political problems.

[D] financial responsibility is an indicator of political status.

第9题:

12 Which of the following statements are correct?

(1) Contingent assets are included as assets in financial statements if it is probable that they will arise.

(2) Contingent liabilities must be provided for in financial statements if it is probable that they will arise.

(3) Details of all adjusting events after the balance sheet date must be given in notes to the financial statements.

(4) Material non-adjusting events are disclosed by note in the financial statements.

A 1 and 2

B 2 and 4

C 3 and 4

D 1 and 3

第10题:

According to the passage, unsecured loans are granted on the basis of ______.

A.the borrower's financial condition

B.the guarantor's financial condition

C.the guarantor's past record of repayment

D.the borrower's pledged assets