第1题:

(c) Discuss the reasons why the net present value investment appraisal method is preferred to other investment

appraisal methods such as payback, return on capital employed and internal rate of return. (9 marks)

第2题:

Rate of return(or return)on capital 资本收益率(或资本收益)

在一项投资或一件资本品上的收益(yield)。比如,一项耗费100美元的投资每年带来12美元的收益,那么这项投资的收益率就是每年12%。

第3题:

Which of the following is referred to as payback period:

A . the number of periods required to recover the initial investment

B . the rate of return on the investment

C . the number of periods required to bring project cost back to the original budget, based on current performance

D . loan payment schedule

E . None of the above

第4题:

第5题:

PV Co is evaluating an investment proposal to manufacture Product W33, which has performed well in test marketing trials conducted recently by the company’s research and development division. The following information relating to this investment proposal has now been prepared.

Initial investment $2 million

Selling price (current price terms) $20 per unit

Expected selling price inflation 3% per year

Variable operating costs (current price terms) $8 per unit

Fixed operating costs (current price terms) $170,000 per year

Expected operating cost inflation 4% per year

The research and development division has prepared the following demand forecast as a result of its test marketing trials. The forecast reflects expected technological change and its effect on the anticipated life-cycle of Product W33.

It is expected that all units of Product W33 produced will be sold, in line with the company’s policy of keeping no inventory of finished goods. No terminal value or machinery scrap value is expected at the end of four years, when production of Product W33 is planned to end. For investment appraisal purposes, PV Co uses a nominal (money) discount rate of 10% per year and a target return on capital employed of 30% per year. Ignore taxation.

Required:

(a) Identify and explain the key stages in the capital investment decision-making process, and the role of

investment appraisal in this process. (7 marks)

(b) Calculate the following values for the investment proposal:

(i) net present value;

(ii) internal rate of return;

(iii) return on capital employed (accounting rate of return) based on average investment; and

(iv) discounted payback period. (13 marks)

(c) Discuss your findings in each section of (b) above and advise whether the investment proposal is financially acceptable. (5 marks)

第6题:

(ii) Briefly discuss TWO factors which could reduce the rate of return earned by the investment as per the

results in part (a). (4 marks)

第7题:

Injectors for use with heavy fuel oil must be cooled by either water or light oil to_____.

A.prevent heat corrosion to internal components

B.increase fuel delivery rate and economy

C.prevent pre-ignition

D.avoid carbonization of the nozzle tips

第8题:

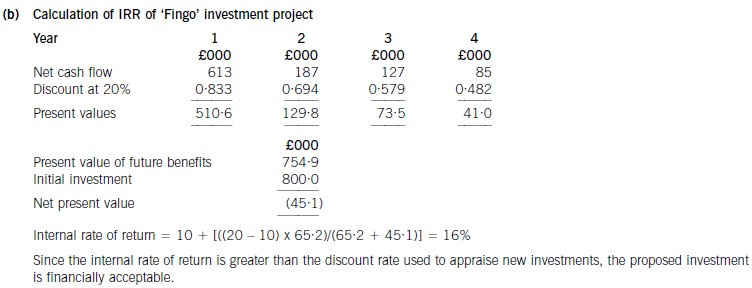

(b) Calculate the internal rate of return of the proposed investment and comment on your findings. (5 marks)

第9题:

第10题: